Downturn refresher: what happens when prices start falling?

When we think about the housing market we tend to focus on when values rise but in the recent past values have fallen in each capital city; this week we look at the magnitude and duration of these falls in the past.

Throughout the past 20 years it has been much more common for combined capital city dwelling values to have been increasing than falling. Although value rises have been more common, it doesn’t mean that the housing market is bulletproof and in some instances values have fallen quite dramatically and rapidly. Typically the Reserve Bank (RBA) or the Government have adjusted fiscal and/or monetary policy to support the housing market and arrest the value falls.

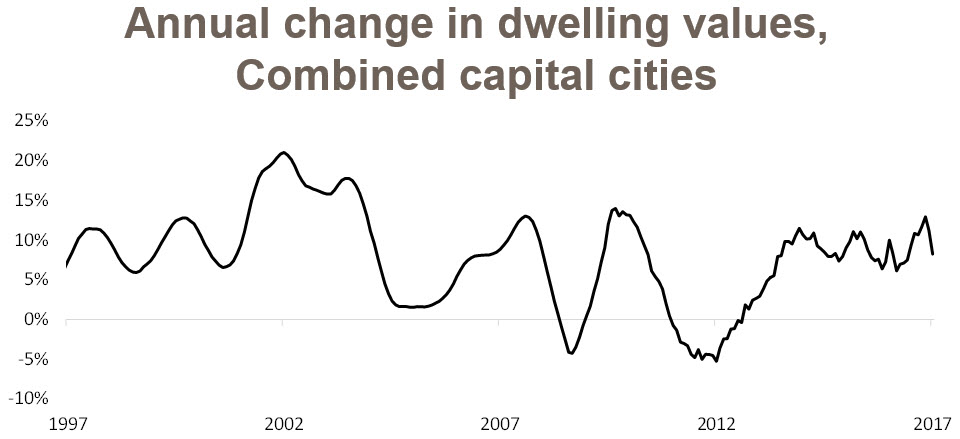

Across the combined capital cities, dwelling values have increased by 346.4% over the 20 years to April 2017. In the two periods in which values have fallen, capital city dwelling values fell by -6.1% between March and December 2008 and they fell by -7.4% between October 2010 and May 2012.

At an individual capital city level housing markets have cycled quite differently however, the majority of capital cities recorded a decline in dwelling values in both 2008 and from late 2010/early 2011. The 2008 decline occurred as the financial crisis hit with values falling however, stimulus measures in the form of aggressive interest rate cuts along with cash handouts and boosts to first home buyer’s grants proved enough to spur demand and turnaround the decline in values.

In 2010 dwelling values fell as the post financial crisis stimulus was being wound out of the market with interest rates increasing and first home buyer incentives being removed. These value falls were arrested as the RBA reversed direction and started to cut official interest rates again in late 2011.

Looking at the declines which commenced in 2008, the magnitude of falls was fairly minor considering most advanced economies fell into recession as a result of the financial crisis. Hobart and Darwin were relatively unaffected by the declines however, Melbourne (-8.3%), Perth (-6.8%) and Sydney (-6.2%) were more impacted than all other capital cities. The period of decline proved quite short and it has become clear that the stimulus measures effectively staved off sharper declines and possibly a national recession.

From 2010 to 2011/12 all capital cities experienced falls in dwelling values as the financial crisis stimulus and low interest rates were wound out of the market. Sydney (-5.0%), Adelaide (-6.9%) and Canberra (-4.4%) were the only capital cities in which values didn’t fall by more than 10% over this period. The largest falls were recorded in Darwin (-19.7%), Hobart (-14.3%) and Brisbane

(-11.7%). Over the period of falls, Darwin (-1.2%) averaged the largest average monthly fall along with Hobart (-0.8%), Melbourne

(-0.6%) and Perth (-0.6%). Across the other capital cities, Sydney, Adelaide and Canberra recorded average declines of -0.3%/month and Brisbane’s declines averaged -0.5%/month.

This analysis serves as a reminder that although capital city dwelling values have largely increased over the past 20 years, they are not immune from potential declines. The impetus for these previous declines have been external economic shocks and the stimulus of low interest rates and grants to first home buyers being removed. We aren’t currently seeing any economic shocks of the size of the 2008 financial crisis but we are seeing unemployment rate at similar levels to 2008/09 and historically high levels of underemployment. The market is also slowly seeing historic low mortgage rates moving higher against a backdrop of record low wages growth and record high household debt. Depending on how much mortgage rates are increased (noting that this is not happening due to the RBA) home owners should be aware that it could lead to a slowing or even some potential falls in dwelling values.

![]()

Source: CoreLogic Feed