Is sentiment, particularly housing sentiment, turning negative?

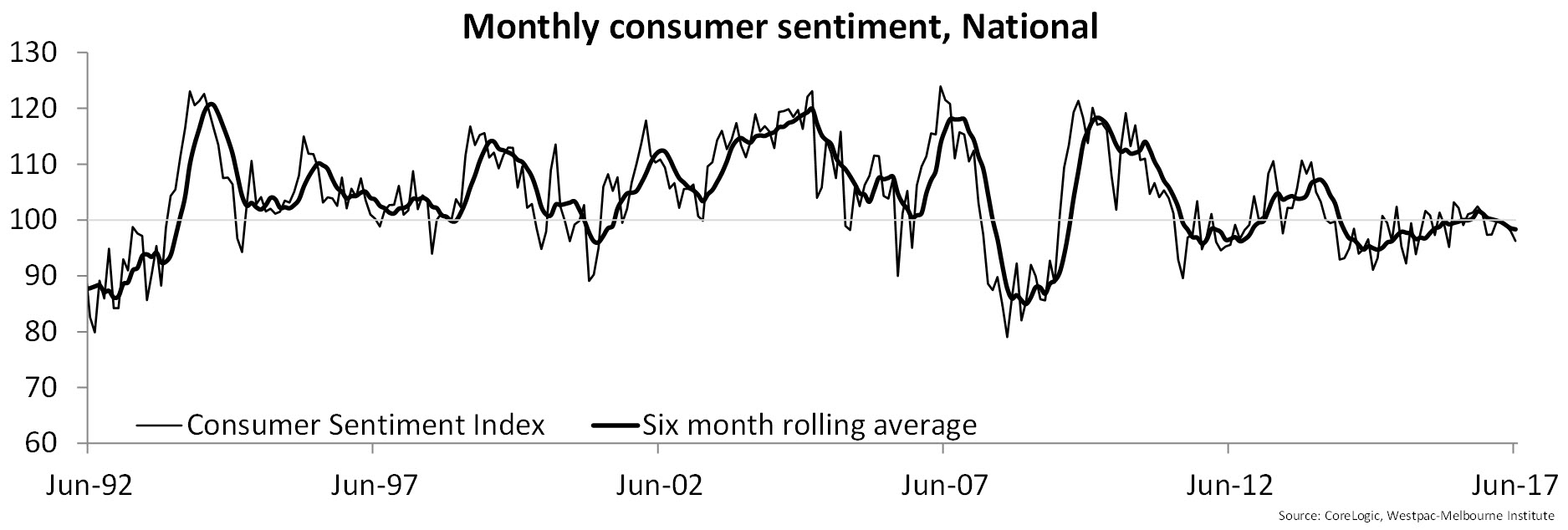

The Westpac and Melbourne Institute’s consumer sentiment index for June 2017 was released earlier this week. The Index was recorded at 96.2 points which was the lowest monthly reading for the index since April 2016.

When the Consumer Sentiment Index sits below 100 points it means that consumers are more pessimistic than optimistic. The Index has now been recorded below 100 points for seven consecutive months which is the longest run of negative sentiment the Index has seen since January 2015.

Before the most recent seven months of negative readings, sentiment had been optimistic for the four months from August to November 2016. Remember that the Reserve Bank (RBA) cut the cash rate by 25 basis points in August 2016. Sentiment was also optimistic between May and June 2016 following a 25 basis point cut in official interest rates in May 2016. Over the previous few years, the only instances in which sentiment would reach optimistic territory coincided with those months in which the RBA cut official interest rates. This would seem to suggest that consumers are extremely sensitive to interest rate movement, which really isn’t a surprise given that household debt is at a record high meaning households are very sensitive to fluctuations in mortgage rates. While there has been no movement in the cash rate since August last year, many lenders have been increasing mortgage rates and it seems that this is feeding into a deterioration of consumer sentiment.

Further highlighting the sensitivity of households to movements in interest rates is the time to buy a dwelling index which is a subset of the consumer sentiment index data. In June 2017 the time to buy a dwelling index was recorded at 90.9 points and although that is slightly higher than over the previous month the time to buy a dwelling index is hovering around the lowest levels seen since the financial crisis. Australians tend to be bullish on housing and its prospects however, this data shows that sentiment towards housing has been consistently negative since February of this year.

Across the states, South Australia is currently the only one in which sentiment towards buying a dwelling is currently trending higher. In the two states which are home to the hottest housing markets, New South Wales and Victoria, on a rolling three month basis sentiment has consistently been more pessimistic than optimistic since March of this year and June of last year respectively. Importantly, as the growth phase in Sydney and Melbourne dwelling values has continued there has been an ongoing sentiment decline. Of course just because sentiment around purchasing homes has declined it hasn’t really stopped the growth in values but with more substantial declines recently perhaps this is signalling a realisation that the value growth has come or is coming to an end.

The quarterly release of consumer sentiment data highlights respondent’s selection for the wisest place for savings and over recent quarters there have been some significant declines in respondents choosing real estate. The June 2017 quarter showed that 13.3% of respondents chose real estate as the wisest place for savings. Of course, real estate isn’t just residential property but there has been a substantial weakening over recent years as highlighted in the above chart. Although June’s result was higher than the March 2017 result, it remains well below recent levels. Despite the moderate quarterly increase, the proportion of respondents choosing real estate as the wisest place for savings is sitting at historically low levels.

The consumer sentiment data is only one set of data suggesting sentiment towards housing may be turning however, it is a timely measure with a good track-record. Furthermore when it is paired with other data there are now a number of data points indicating weaker housing conditions. These include but are not limited to:

- Monthly building approvals having fallen well below recent peak levels

- The total value of housing finance commitments have eased, particularly for investors

- Migration data showing that migration away from Sydney has accelerated which is likely a result of deteriorating housing affordability

- The monthly change in housing credit growth slowing, particularly for investor housing

- Auction clearance rates having eased from recent highs in both Sydney and Melbourne

- In Sydney there has also been a noticeable increase in the number of properties advertised for sale relative to a year ago

- Lenders have been increasing mortgage rates; more so for investors but owner occupier rates have also increased.

As time progress there is mounting evidence that housing markets, particularly Sydney which has been the hottest, have lost momentum. The consumer sentiment data is also supporting the notion of a cooler housing market and we are growing increasingly confident that the housing market is at or extremely close to its peak if not slightly past the peak already.

![]()

Source: CoreLogic Feed